uae-vatfiling.com

Input VAT Recovery in UAE: Rules, Restrictions & Practical Examples

Learn how input VAT recovery works in the UAE. Understand rules, restrictions, and practical examples. Get expert VAT guidance to maximize recovery.

Gupta Group International

1/9/20266 min read

Input VAT Recovery in UAE: Rules, Restrictions & Practical Examples

Input VAT Recovery in UAE: Rules, Restrictions & Practical Examples :

Value Added Tax (VAT) in the UAE has become an integral part of doing business since its introduction on 1 January 2018 at a standard rate of 5%. While VAT is straightforward in concept — collect tax on sales and remit to the Federal Tax Authority (FTA) — the reality can be much more complex when it comes to recovering Input VAT.

For businesses, the ability to recover VAT paid on business purchases (Input VAT) is vital for maintaining profitability and cash flow. However, not all VAT paid on purchases is recoverable. Knowing when, how much, and under what conditions Input VAT can be reclaimed sets compliant businesses apart from those at risk of penalties or disallowed deductions.

This comprehensive guide dives deep into Input VAT recovery in the UAE, including applicable rules, restrictions, documentation requirements, and practical examples. Whether you’re a VAT-registered SME, an accountant, or a multinational operating in the UAE, this article will equip you with the insights needed to confidently manage VAT claims.

What Is Input VAT Recovery ?

Input VAT is the VAT your business pays on purchases of goods and services that it uses to generate taxable supplies.

When a business makes taxable sales, it charges Output VAT to customers. The VAT system allows you to offset Output VAT with Input VAT, meaning:

VAT Payable = Output VAT – Recoverable Input VAT

If Input VAT exceeds Output VAT in a tax period, you may have a VAT refund or carry forward the credit to the next period.

Input VAT recovery is the mechanism through which VAT-registered businesses recover the VAT they’ve paid on eligible purchases. However, only VAT that meets specific criteria can be reclaimed.

Conditions for Input VAT Recovery :

To recover Input VAT in the UAE, the following conditions must be satisfied:

A. VAT Registration :

Your business must be registered for VAT with the FTA. Unregistered entities cannot claim Input VAT.

B. Business Purpose :

Input VAT can only be recovered on expenses used for making taxable supplies — i.e., supplies subject to VAT at either the standard 5% rate or zero rate.

If a purchase relates to exempt supplies, Input VAT cannot be claimed.

C. Valid Tax Invoice

The business must hold a valid tax invoice issued by a VAT-registered supplier. Cash receipts or regular invoices without VAT details are insufficient.

D. Proper Accounting Records

Accurate accounting records must be maintained and match the Input VAT claimed in your VAT return.

E. Timing of Claim

Input VAT should be claimed in the VAT return relating to the tax period in which the purchase was made, provided the invoice is received by the return’s due date.

General Restrictions on Input VAT Deduction :

Even when the general conditions above are met, there are several common restrictions where UAE VAT law disallows or limits input VAT recovery:

A. Exempt Supplies

If a business makes only exempt supplies, it cannot recover Input VAT related to those supplies.

Example: Financial services that are exempt from VAT mean the Input VAT on related expenses is non-recoverable.

B. Non-Business Purposes

Input VAT paid on purchases for personal or non-business use cannot be reclaimed.

Example: VAT on personal travel or entertainment unrelated to business activity.

C. Certain Business Activities

Some activities, while business in nature, have limited or no input VAT recovery due to specific restrictions.

These include:

Entertainment expenses

Employee personal benefits

Club memberships

Imported goods used for exempt supplies

D. Fashioning of Non-Taxable Goods

If goods are produced exclusively for exempt sales or non-business purposes, Input VAT related to those inputs is not recoverable.

Special Cases and Exceptions :

Some cases require deeper scrutiny because the general rules don’t always apply straightforwardly.

A. Vehicles and Transportation :

Input VAT on vehicles used exclusively for business may be recoverable. However:

Input VAT on passenger vehicles used for mixed purposes is often restricted.

VAT on commercial vehicles (used solely for business) is generally recoverable.

B. Entertainment Expenses

Input VAT on entertainment (meals, events, hospitality) is restricted unless directly related to a business-to-business interaction and supported by documentation.

C. Imported Goods & Customs VAT

When goods are imported into the UAE, customs duty and import VAT are payable. Input VAT on import can be recovered if the import qualifies as a business expense and proper documentation is retained.

Input VAT Recovery for Mixed-Use Expenses :

Many businesses incur expenses that are used for both taxable and non-taxable purposes (“mixed use”). In such cases, only the portion related to taxable supplies can be claimed.

Example Formula for Allocation

If a purchase is partly for business (taxable) and partly for exempt or personal use:

Recoverable VAT = Total VAT × (Taxable Use / Total Use)

Example:

An advertising expense of AED 10,000 includes VAT of AED 500, and 70% of the advertising directly supports taxable sales:

Recoverable Input VAT = 500 × 0.70 = AED 350

Only AED 350 can be reclaimed.

Input VAT and Capital Assets :

Capital assets (vehicles, machinery, equipment, buildings) require special attention:

If a capital asset is used entirely for taxable supplies, full Input VAT recovery is allowed.

If it has mixed use (taxable + exempt), partial recovery applies based on actual use.

If used solely for exempt supplies, Input VAT cannot be recovered.

Adjustments Over Time

For assets used over multiple periods, UAE VAT law may require adjustments if the use changes over time. For example:

A business initially uses machinery for taxable supplies (100% recoverable), but later switches to exempt use — adjustments are necessary.

Input VAT Recovery in Free Zones :

UAE Free Zones (e.g., DMCC, JAFZA, DIFC, IFZA) present unique scenarios :

A. Designated vs Non-Designated Zones

Designated Zones (e.g., JAFZA, RAKEZ) are treated as outside the UAE for VAT on goods.

Non-Designated Zones (e.g., DIFC, ADGM, some services) follow normal VAT rules.

Input VAT on goods and services in Free Zones must be analyzed under special rules, especially related to place of supply, customs status, and type of transaction.

B. Example: VAT on Imports into Free Zones

If goods are imported into a designated zone and remain there, VAT may not be immediately due — impacting when Input VAT can be reclaimed.

In contrast, imports into non-designated zones follow regular import VAT rules.

C. Services in Free Zones

Input VAT on services received by businesses in Free Zones is recoverable when those services support taxable outputs, even if the place of supply rules are complex.

Documentation & Record-Keeping Requirements :

To support Input VAT claims, businesses must maintain:

A. Valid Tax Invoices

Supplier’s name, TRN, and address

Customer’s name

Invoice date and number

Description of goods/services

VAT amount

B. Contracts & Supporting Documents

Contracts, agreements, delivery notes, import declarations, and proof of payment help validate the business purpose and timing of expenses.

C. Proper Accounting Records

Accurate accounting is essential. Electronic systems are recommended to match Input VAT claims with the general ledger.

Records must be kept for at least 5 years to comply with FTA requirements.

Practical Examples of Input VAT Recovery :

Example 1: Office Supplies

Business buys office supplies for AED 2,000 (VAT 5% = AED 100)

Supplies used entirely for taxable sales

Result: Full VAT (AED 100) is recoverable.

Example 2: Employee Travel

Company pays for employee personal travel unrelated to business for AED 10,000 (VAT 5% = AED 500)

Result: Input VAT (AED 500) is not recoverable.

Example 3: Mixed-Use Vehicle

Company purchases a vehicle for AED 100,000 (VAT 5,000), used 60% for business and 40% personal.

Recoverable VAT: 5,000 × 0.60 = AED 3,000

Example 4: Import VAT on Goods

Import VAT of AED 20,000 is paid on goods that will be sold in taxable supply.

Result: Import VAT is recoverable as Input VAT, provided all documentation is available.

Example 5: Marketing Services for Taxable & Exempt Sales

Marketing agency invoice AED 15,000 (VAT 750). Business uses campaign 80% for taxable services and 20% for exempt.

Recoverable VAT: 750 × 0.80 = AED 600

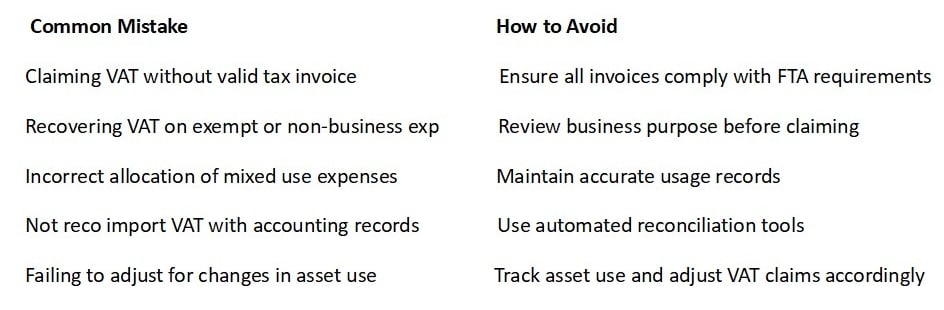

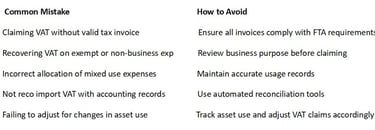

Common Mistakes and How to Avoid Them :

Penalties & Risks for Incorrect Claims :

Incorrect Input VAT claims can lead to :

Penalties for underpayment of VAT

Interest on unpaid amounts

FTA audits and assessments

Reputational risk with regulatory authorities

To avoid these risks, it’s crucial to implement robust VAT compliance processes and periodic internal checks.

How UAE-VATFiling.com Supports Input VAT Recovery :

At uae-vatfiling.com, we specialize in VAT compliance and optimization, including:

✅ End-to-end VAT return preparation

✅ Input VAT reconciliation and advisory

✅ Review of invoices and supporting documentation

✅ Assistance with import VAT and Free Zone scenarios

✅ VAT health checks and audit readiness

Our expert team ensures that your business recovers all legitimate Input VAT while minimizing risk and maximizing compliance efficiency.

Recovering Input VAT in the UAE can dramatically enhance your business’s cash flow, but it requires a thorough understanding of VAT law, careful documentation, and proper accounting practices.

To successfully claim Input VAT:

Ensure VAT registration

Keep valid tax invoices

Claim only for business-related taxable expenses

Apply allocation rules for mixed-use costs

Maintain compliant records for FTA review

With proper systems in place and expert support from uae-vatfiling.com, your business can confidently navigate UAE VAT regulations and optimize its tax position.

© 2026 uae-vatfiling.com